Retirement Planning for Freelancers in Their 40s and 50s: It Is Not Too Late

If you are a freelancer in your 40s or 50s who has not yet built significant retirement savings, you are not alone — and it is absolutely not too late to build meaningful retirement wealth. The combination of high contribution limits for self-employed retirement accounts, powerful catch-up contribution provisions, and the income-generating potential of an established freelance career means that this decade is one of the most financially productive periods in a freelancer’s life.

What is true is that you need to be intentional, aggressive, and strategic. You do not have the luxury of decades of compound growth that younger savers enjoy, but you do have higher income, lower fixed expenses in many cases (mortgage possibly paid down, children potentially grown), and access to retirement account limits that dwarf what employees can contribute. This guide shows you exactly how to use all of these advantages.

Understanding Where You Stand

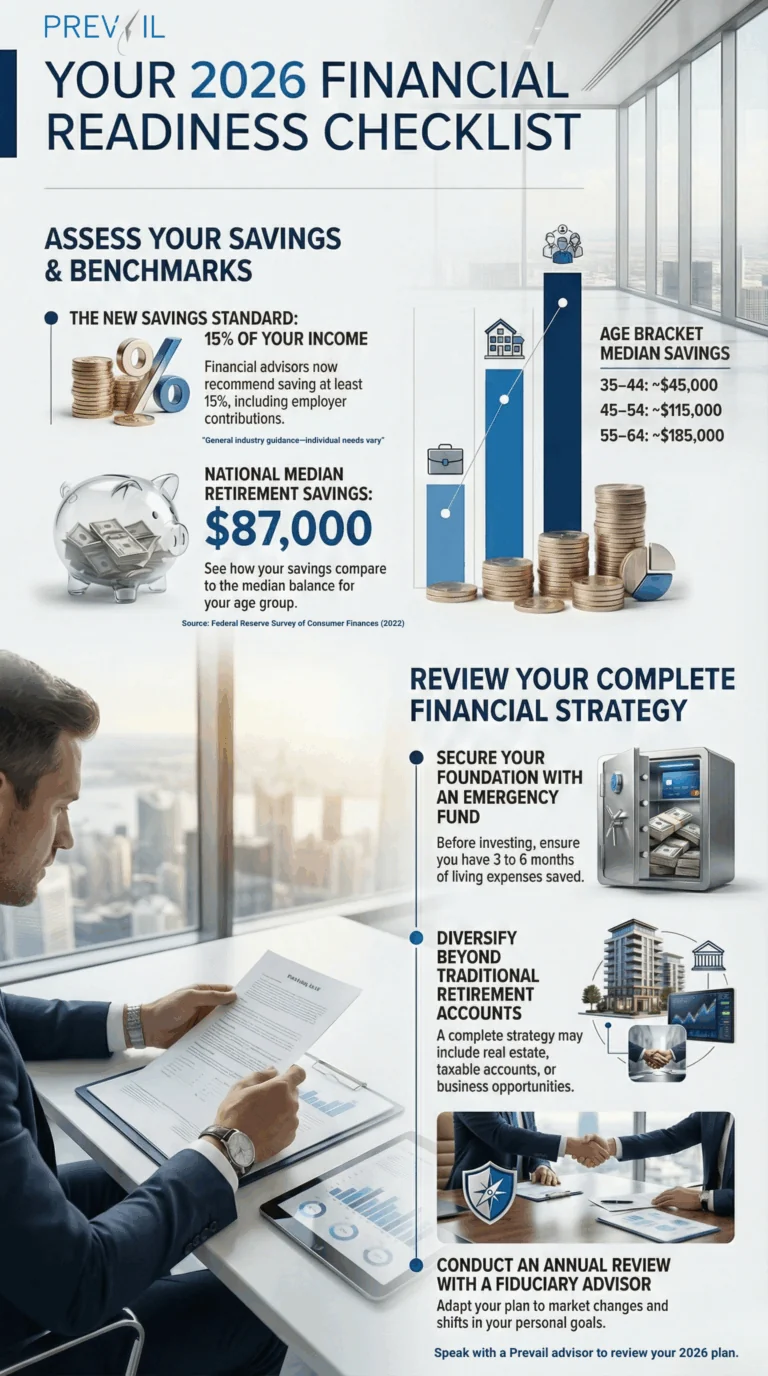

Before making any changes, you need a clear picture of your current situation. Calculate your net worth: total assets (savings, investments, home equity, retirement accounts) minus total liabilities (mortgage, student loans, credit card debt, other debts). This is your financial baseline.

Then use the 25x rule to estimate your retirement savings target: multiply your expected annual retirement spending by 25. If you expect to spend $70,000 per year in retirement and your current retirement accounts total $150,000, you have a gap of $1,600,000 to close over your remaining working years.

Do not be discouraged by a large gap. A freelancer who is 45 and earns $120,000 per year can contribute up to $58,000 per year to a Solo 401(k) in 2026. Doing so consistently for 20 years with a 7 percent average return produces over $2,500,000. The math works — but it requires starting now and being consistent.

The Catch-Up Contribution Advantage

Starting at age 50, the IRS allows additional catch-up contributions to retirement accounts specifically designed to help late starters accelerate their savings. These are among the most valuable provisions in the tax code for freelancers in their 50s.

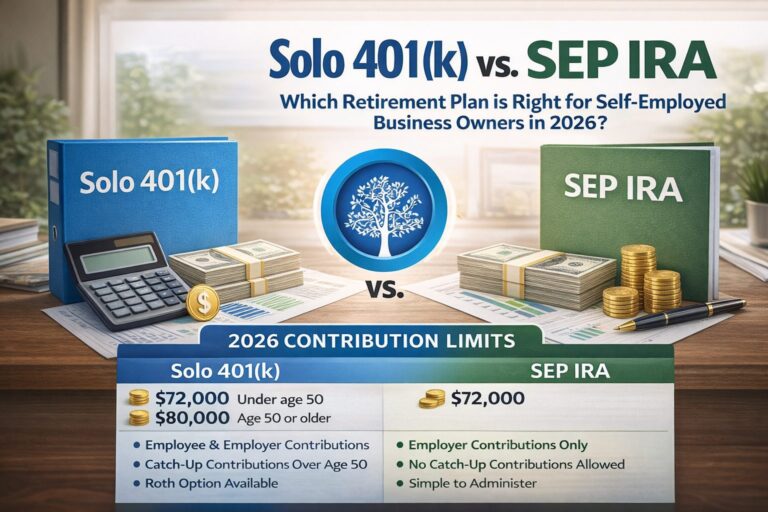

Solo 401(k) catch-up: $7,500 additional employee contribution per year (on top of the standard $23,000), for a total employee contribution of $30,500. Combined with the employer contribution of up to 25 percent of net self-employment income, a 55-year-old freelancer with $120,000 in net income could potentially shelter over $58,000 from taxes in a single year.

IRA catch-up: $1,000 additional contribution per year to a Traditional or Roth IRA (total of $8,000 per year at 50+).

HSA catch-up: $1,000 additional contribution per year to an HSA starting at age 55 (total of $5,150 for individual coverage in 2026).

Combining all three — maxing out a Solo 401(k), making a full Roth IRA contribution, and maximizing HSA contributions — a 55-year-old freelancer could potentially shelter over $65,000 from taxes in a single year. That is an extraordinary wealth-building opportunity.

→ SEP-IRA vs Solo 401(k) for Freelancers

Aggressive Savings Strategies for Your 40s and 50s

The Income Acceleration Strategy

Your 40s and 50s are typically your highest-earning years as a freelancer. You have a reputation, an established client base, and the experience to command premium rates. Rather than lifestyle inflating as your income grows, direct the additional income directly to retirement accounts. Every rate increase, every new client, and every upsell should first fund retirement — then lifestyle.

→ How to Set Your Freelance Rates in the US

The Expense Audit

As you approach retirement, reducing fixed monthly expenses has two benefits: it lowers the amount you need to save (a lower lifestyle cost means a smaller retirement target) and it frees up current cash flow for additional retirement contributions. Review every recurring expense and eliminate or reduce anything that does not provide meaningful value to your life.

The S-Corporation Strategy

At income levels above $60,000 to $80,000 in net profit, converting your LLC to be taxed as an S-Corporation can reduce your self-employment tax significantly. By paying yourself a reasonable salary and taking the remainder as distributions, you only pay payroll taxes on the salary portion. The savings — potentially $5,000 to $15,000 per year at common freelance income levels — can be redirected entirely to retirement accounts.

This strategy requires setting up payroll, filing quarterly payroll tax returns, and working with a CPA — but for freelancers earning $100,000 or more per year, the tax savings typically justify the additional complexity many times over.

→ LLC vs Sole Proprietorship for Freelancers

Planning Your Healthcare Bridge

One of the most significant challenges for freelancers who want to retire before 65 is health insurance. Medicare eligibility begins at 65. If you retire at 58, you face seven years of self-funded health insurance at ages when premiums are highest.

Strategies for managing this gap include maintaining ACA Marketplace coverage (potentially with significant subsidies if your retirement income is modest), contributing heavily to an HSA while still working to build a tax-free medical fund, considering part-time freelance work that generates enough income to qualify for ACA subsidies while keeping you engaged professionally, and factoring healthcare costs explicitly into your retirement income projections.

→ Health Insurance for Freelancers Over 50 → What Is an HSA and Should Freelancers Use One?

Social Security Optimization

The age at which you begin claiming Social Security benefits dramatically affects your monthly payment. Benefits claimed at 62 (the earliest possible age) are permanently reduced by approximately 30 percent compared to claiming at your full retirement age (67 for most people born after 1960). Delaying to age 70 increases your benefit by 8 percent per year beyond full retirement age — a total of approximately 24 percent more than at 67.

For freelancers with adequate savings, delaying Social Security as long as possible — ideally to 70 — and drawing down retirement accounts in the interim is often the optimal strategy. The guaranteed 8 percent annual increase from delaying is a return that no investment can reliably match.

Working With a Financial Planner

For freelancers in their 40s and 50s with significant assets and complex decisions ahead — Social Security timing, Medicare planning, sequence of returns risk, estate planning — working with a fee-only fiduciary financial planner is worth serious consideration. Fee-only planners charge for their time rather than earning commissions on products they sell, which aligns their incentives with yours.

Look for a CFP (Certified Financial Planner) with experience working with self-employed clients. A comprehensive financial plan typically costs $2,000 to $5,000 and can save many times that amount in optimized decisions over the years ahead.

→ Best Retirement Plans for Self-Employed Americans → How Much Should a Freelancer Save for Retirement? → Freelance Financial Planning Checklist → Complete Freelance Finance Guide