Best Retirement Plans for Self-Employed Americans in 2026

One of the most significant financial advantages of being self-employed in the United States is access to retirement accounts with dramatically higher contribution limits than what standard employees can use. While a traditional employee is limited to $23,000 per year in a 401(k) contribution, a self-employed individual with the right structure can shelter $69,000 or more from taxes in a single year. For a freelancer in a 24 percent federal tax bracket, maxing out a Solo 401(k) represents over $16,000 in immediate federal tax savings alone.

Yet despite these advantages, surveys consistently show that self-employed Americans save less for retirement than their employed peers. The primary reason is not income — it is the absence of automatic enrollment and employer matching that makes retirement saving invisible and effortless for employees. As a freelancer, you have to build that system yourself. This guide gives you everything you need to choose the right account, understand the contribution limits, and start building real retirement wealth.

Why Retirement Planning Is More Urgent for Freelancers

There are three reasons retirement planning is more critical — and more complex — for freelancers than for employees.

First, there is no employer match. The average employer 401(k) match is 4.7 percent of salary. On a $80,000 income, that is $3,760 per year in free money that employees receive automatically. As a freelancer, every dollar in your retirement account comes from you.

Second, there is no automatic enrollment. Employees are increasingly enrolled in retirement plans by default and must opt out to stop contributing. Freelancers must actively choose to save, set up accounts, and make contributions — all of which require ongoing intentional action.

Third, Social Security benefits for freelancers are often lower than for employees because self-employment income fluctuates. Years with low income mean lower lifetime Social Security benefits. Your personal retirement savings must compensate for this gap.

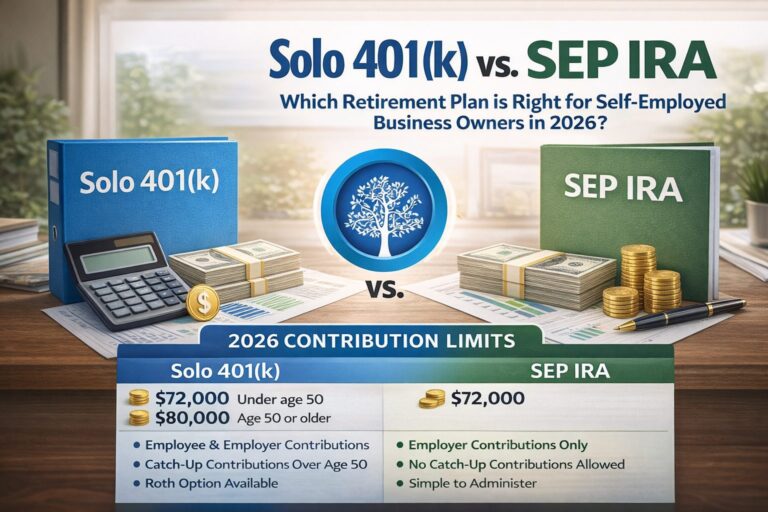

Option 1: SEP-IRA — The Simplest High-Limit Account

The SEP-IRA (Simplified Employee Pension Individual Retirement Account) is the most popular retirement account for self-employed Americans, and for good reason: it combines very high contribution limits with almost zero administrative complexity.

How Much Can You Contribute?

For 2026, you can contribute up to 25 percent of your net self-employment income to a SEP-IRA, with a maximum contribution of $69,000. Net self-employment income is your gross freelance income minus business expenses and the deductible portion of self-employment tax. In practice, this works out to approximately 18.59 percent of your gross self-employment income.

Examples at different income levels:

- $50,000 gross income: approximately $9,295 maximum SEP-IRA contribution

- $100,000 gross income: approximately $18,590 maximum SEP-IRA contribution

- $200,000 gross income: approximately $37,180 maximum SEP-IRA contribution

- $370,000+ gross income: maximum contribution of $69,000

Setup and Administration

Opening a SEP-IRA is remarkably simple. You can open one at any major brokerage — Fidelity, Vanguard, Schwab, or TD Ameritrade — in less than 30 minutes with no fees. There are no annual filings required unless your account balance exceeds $250,000. You can make contributions at any time during the year and as late as your tax filing deadline, including extensions — meaning you have until October 15 of the following year if you file a six-month extension.

Investment Options

A SEP-IRA offers the same investment options as a Traditional IRA: stocks, bonds, mutual funds, ETFs, REITs, and more. Most freelancers invest in low-cost index funds from providers like Vanguard or Fidelity for broad market exposure with minimal fees.

The Tax Treatment

SEP-IRA contributions are fully tax-deductible in the year you make them, reducing your adjusted gross income dollar for dollar. The investments grow tax-deferred, meaning you pay no taxes on dividends, interest, or capital gains until you withdraw the money in retirement. Withdrawals in retirement are taxed as ordinary income.

Option 2: Solo 401(k) — The Most Powerful Option for Most Freelancers

The Solo 401(k) — also called an Individual 401(k), Self-Employed 401(k), or i401(k) — is arguably the most powerful retirement account available to self-employed individuals who have no employees other than a spouse. It combines the high contribution limits of a SEP-IRA with the unique ability to make employee-style contributions regardless of income level.

The Two-Part Contribution Structure

What makes the Solo 401(k) uniquely powerful is that you wear two hats simultaneously: you are both the employee and the employer. This allows two separate types of contributions:

Employee elective deferral: As the employee, you can contribute up to $23,000 in 2026, regardless of what percentage of your income that represents. If you are 50 or older, you can make an additional $7,500 catch-up contribution, bringing the employee total to $30,500.

Employer profit-sharing contribution: As the employer, you can contribute up to 25 percent of your net self-employment income (the same percentage as a SEP-IRA). This contribution is in addition to your employee contribution.

The combined total of employee plus employer contributions cannot exceed $69,000 in 2026 ($76,500 with catch-up contributions).

Why the Solo 401(k) Wins at Lower Income Levels

At lower income levels, the Solo 401(k) allows dramatically higher contributions as a percentage of income compared to the SEP-IRA.

Example with $40,000 in net self-employment income:

- SEP-IRA maximum: approximately $7,436 (18.59 percent of $40,000)

- Solo 401(k) maximum: $23,000 employee contribution alone (limited to earned income, but far exceeds the SEP-IRA limit)

For a freelancer with $40,000 in income who wants to maximize retirement savings and minimize current taxes, the Solo 401(k) is decisively superior.

The Roth Option

Many Solo 401(k) providers offer the ability to designate employee contributions as Roth contributions. Roth contributions are made with after-tax dollars, grow tax-free, and are withdrawn tax-free in retirement. This is the only self-employment retirement account that offers a Roth contribution option at the same high limits. For younger freelancers or those expecting to be in a higher tax bracket in retirement, the Roth Solo 401(k) is a powerful wealth-building tool.

Setup Requirements

Unlike the SEP-IRA, a Solo 401(k) must be established by December 31 of the tax year for which you want to make contributions. You can make the actual contributions up to your filing deadline, but the plan document must exist before year-end. Most major brokerages provide the plan documents as part of account opening — Fidelity, Vanguard, and Charles Schwab all offer free Solo 401(k) accounts with excellent investment options.

→ SEP-IRA vs Solo 401(k): Which Is Better for Freelancers?

Option 3: SIMPLE IRA

The SIMPLE IRA (Savings Incentive Match Plan for Employees) is designed primarily for small businesses with employees but can also be used by sole proprietors with no employees. The employee contribution limit for 2026 is $16,000, with a $3,500 catch-up for those 50 and older. Employer contributions are required — either a 2 percent contribution for all eligible employees or a 3 percent matching contribution.

For most solo freelancers, the SIMPLE IRA is less attractive than either the SEP-IRA or Solo 401(k) because of its lower contribution limits and mandatory employer contribution requirements. However, if you have employees and want a retirement plan for your team, the SIMPLE IRA is worth considering.

Option 4: Traditional and Roth IRA

Any self-employed person can contribute to a Traditional or Roth IRA in addition to their primary self-employment retirement account. The contribution limit is $7,000 for 2026, with an additional $1,000 catch-up for those 50 and older.

A Traditional IRA contribution is tax-deductible if your income falls below certain thresholds ($77,000 for single filers in 2026 if covered by a workplace plan; as a freelancer with no workplace plan, you can always deduct Traditional IRA contributions regardless of income). A Roth IRA provides tax-free growth and tax-free withdrawals in retirement and phases out at incomes above $146,000 for single filers.

Most financial planners recommend maxing out your primary self-employment account first (SEP-IRA or Solo 401(k)) and then adding a Roth IRA contribution for tax diversification.

→ Roth IRA for Freelancers: Is It Worth It in 2026?

Comparing All Four Options Side by Side

SEP-IRA: Best for simplicity. Contribution limit tied to income percentage. No Roth option. No loans. Setup anytime before filing deadline.

Solo 401(k): Best for maximum contributions at all income levels. Roth option available. Loans may be available. Must establish by December 31.

SIMPLE IRA: Best for small businesses with employees. Lower contribution limits. Mandatory employer contributions.

Traditional/Roth IRA: Best as a supplement to primary accounts. Lowest contribution limits. Most flexible withdrawal rules for Roth contributions.

The Single Most Important Step: Start Now

The most powerful force in retirement savings is time. A freelancer who invests $500 per month starting at age 30 and earns an average annual return of 7 percent will have approximately $1,197,000 at age 65. A freelancer who waits until 40 to start the same monthly investment will have approximately $567,000 — less than half — despite contributing for 25 years rather than 35.

Open your account today. Contribute whatever you can afford. Increase your contribution rate as your income grows. The specific account type matters far less than the habit of consistent saving.

→ How Much Should a Freelancer Save for Retirement? → What Is Self-Employment Tax and How to Calculate It → Best Tax Deductions for Freelancers → Complete Freelance Finance Guide