How to Start Saving for Retirement as a New Freelancer: A Step-by-Step Action Plan

Many new freelancers put retirement savings on the back burner, telling themselves they will start once their income stabilizes, once they pay off debt, or once they land that next big client. This is understandable — starting a freelance business involves countless competing financial priorities. But the cost of delay is enormous and irreversible.

A freelancer who starts saving $500 per month at age 25 and earns a 7 percent average annual return will have approximately $1,444,000 at age 65. A freelancer who waits until 35 to start the same savings habit will have approximately $681,000 — less than half — despite contributing for 30 years rather than 40. The decade of delay costs nearly $763,000 in final portfolio value. That is the price of waiting.

This guide provides a concrete, actionable plan for new freelancers who want to start saving for retirement immediately — even on a modest income.

Before Retirement Savings: The Prerequisites

Starting retirement savings before handling these two priorities is a mistake:

Emergency Fund First: Without a cash cushion of three to six months of essential expenses, every unexpected bill or slow business period becomes a potential retirement account withdrawal. Early withdrawals from retirement accounts trigger income tax plus a 10 percent penalty — a brutal cost. Build your emergency fund before directing money to retirement accounts.

→ Emergency Fund for Freelancers: How Much Do You Need?

Tax System Second: Ensure your quarterly estimated tax payment system is functioning before saving for retirement. The IRS has no interest in waiting — they charge penalties for late quarterly payments regardless of your retirement savings progress. Set aside 25 to 30 percent of every payment received for taxes before anything else.

→ How to Pay Quarterly Taxes as a Freelancer

Once these two are in place, you are ready to start retirement saving.

Step 1: Choose Your First Retirement Account

For most new freelancers, the Roth IRA is the ideal starting point for three reasons:

Simplicity: You can open a Roth IRA in 15 minutes at Fidelity, Vanguard, or Schwab. There is no plan document, no annual filing, and no complexity.

Flexibility: Roth IRA contributions — not earnings — can be withdrawn at any time without tax or penalty. This provides a safety net while you are still building your business.

Tax-free growth: The tax-free compounding of a Roth IRA is most valuable when you have decades ahead of you. Starting a Roth IRA young maximizes the power of tax-free compounding.

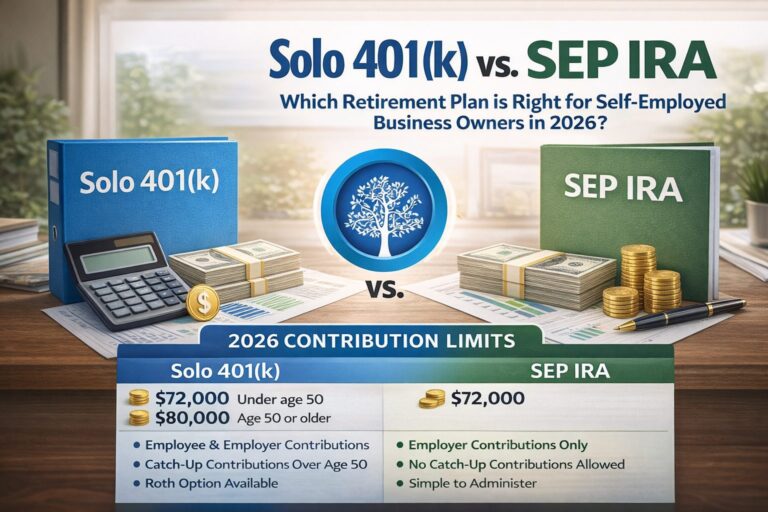

Contribute up to $7,000 per year ($583 per month). As your income grows, add a SEP-IRA or Solo 401(k) alongside your Roth IRA for significantly higher contribution capacity and larger current-year tax deductions.

→ Roth IRA for Freelancers: Is It Worth It?

Step 2: Open Your Account at the Right Brokerage

The three most freelancer-friendly brokerages for retirement accounts in 2026 are:

Fidelity: No account fees, no minimum balance, excellent low-cost index funds, outstanding customer service, and a best-in-class Solo 401(k) with Roth option and no fees.

Vanguard: The pioneer of low-cost index fund investing. No fees on most accounts. Slightly less user-friendly interface than Fidelity but with exceptional investment options and a long reputation for putting investors first.

Charles Schwab: No fees, no minimums, excellent app, and a strong Solo 401(k) offering. A great all-around choice for freelancers who want simplicity.

Avoid brokerages that charge annual account fees or have limited investment options. The expense ratios on your investments matter enormously over decades — a 1 percent annual fee versus a 0.05 percent fee on a $500,000 portfolio costs you $4,750 per year in performance drag.

Step 3: Choose Your Investments

Investment selection intimidates many new retirement savers, but the research is clear: simple, low-cost, diversified index funds outperform the vast majority of actively managed funds over long time periods. You do not need to be a sophisticated investor to build excellent retirement wealth.

Option A: Target-Date Fund (Simplest) A target-date fund is a single all-in-one investment that automatically maintains a diversified mix of stocks and bonds and gradually shifts to a more conservative allocation as you approach retirement. Choose the fund with the year closest to your expected retirement year. Fidelity Freedom Index 2055, Vanguard Target Retirement 2055, and Schwab Target 2055 are all excellent low-cost options.

Option B: Three-Fund Portfolio (Slightly More Involved) Invest in three index funds: a US total stock market fund, an international stock market fund, and a US bond market fund. A common starting allocation for someone in their 30s is 70 percent US stocks, 20 percent international stocks, and 10 percent bonds. Adjust the bond percentage upward as you age.

Step 4: Automate Your Contributions

The single most powerful thing you can do for your retirement savings is automate them. Set up an automatic monthly transfer from your bank account to your retirement account on a fixed date — ideally a day or two after your average payment receipt date.

Treat this transfer as a non-negotiable bill, just like rent. When you automate savings, you remove the decision point entirely. You never have to remember, never have to resist the temptation to skip a month, and never accidentally spend money you intended to save.

Step 5: Increase Your Contribution Rate Systematically

Do not wait until you feel rich enough to start saving meaningfully. Start with whatever you can — even $100 per month — and commit to increasing your contribution by a specific amount every six months or every time you land a new significant client.

A concrete commitment might be: “Every time I add a recurring client, I will increase my retirement contribution by $100 per month.” Or: “Each January, I will increase my monthly contribution by 10 percent.” Small, systematic increases compound dramatically over a career.

Step 6: Add a SEP-IRA or Solo 401(k) as Your Income Grows

Once your income reaches a level where you can contribute more than $7,000 per year (the Roth IRA limit), add a SEP-IRA or Solo 401(k). These accounts offer dramatically higher contribution limits and provide larger immediate tax deductions — which become increasingly valuable as your income and tax bracket rise.

A common progression for freelancers:

- Years 1-2 (income $30,000 to $50,000): Roth IRA only

- Years 3-5 (income $50,000 to $100,000): Roth IRA + SEP-IRA or Solo 401(k)

- Year 5+ (income $100,000+): Max out Solo 401(k) + Roth IRA

→ Best Retirement Plans for Self-Employed Americans → SEP-IRA vs Solo 401(k) for Freelancers → How Much Should a Freelancer Save for Retirement? → Complete Freelance Finance Guide