Roth IRA for Freelancers: Is It Worth It in 2026?

The Roth IRA is one of the most beloved accounts in personal finance for good reason: contributions grow completely tax-free, qualified withdrawals in retirement are entirely tax-free, and the account offers flexibility that no other retirement vehicle matches. For freelancers, the Roth IRA serves as an excellent complement to a SEP-IRA or Solo 401(k), providing tax diversification and liquidity that pre-tax accounts alone cannot offer.

But is a Roth IRA worth contributing to when you already have access to high-limit self-employment retirement accounts? The answer for most freelancers is a clear yes — and this guide explains exactly why, when, and how to use one.

How the Roth IRA Works

You contribute after-tax dollars to a Roth IRA — there is no deduction going in. But your contributions and all earnings grow without being taxed year over year. When you withdraw money in retirement — after age 59½ with the account open for at least five years — you pay absolutely zero tax on the entire withdrawal, including decades of investment growth.

For a freelancer who contributes $7,000 per year for 30 years and earns an average annual return of 7 percent, the account would grow to approximately $694,000. Every dollar of that is yours tax-free in retirement. With a pre-tax account, you would owe income tax on every dollar you withdraw.

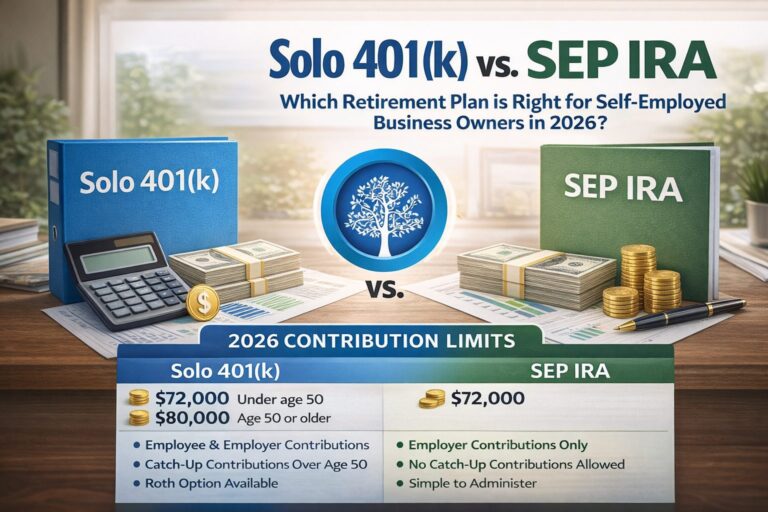

2026 Roth IRA Contribution Limits

- Under age 50: $7,000 per year

- Age 50 and older: $8,000 per year (including $1,000 catch-up contribution)

You must have earned income at least equal to your contribution amount. As a freelancer, your net self-employment income qualifies as earned income.

Income Limits for Direct Roth IRA Contributions

The ability to contribute directly to a Roth IRA phases out at higher income levels. For 2026:

- Single filers: Phase-out begins at $146,000, eliminated at $161,000

- Married filing jointly: Phase-out begins at $230,000, eliminated at $240,000

If your income exceeds these limits, you cannot make direct Roth IRA contributions. However, you can use the backdoor Roth IRA strategy.

The Backdoor Roth IRA: For Higher-Income Freelancers

The backdoor Roth is a perfectly legal two-step process that allows higher-income freelancers to make Roth contributions regardless of income:

Step 1: Make a non-deductible Traditional IRA contribution (up to $7,000). Step 2: Convert the Traditional IRA to a Roth IRA. Because the contribution was non-deductible, there is no additional tax on the conversion (assuming no other pre-tax IRA balances exist — the pro-rata rule can complicate this if you have other Traditional IRA funds).

The backdoor Roth strategy requires careful execution and record-keeping, but it is widely used and IRS-acknowledged. If you have a significant SEP-IRA balance, consult a CPA before attempting a backdoor Roth, as the pro-rata rule may create unexpected taxable income.

Why Freelancers Should Prioritize Tax Diversification

Most freelancers who contribute to a SEP-IRA or traditional Solo 401(k) are building a 100 percent pre-tax retirement portfolio. Every dollar they withdraw in retirement will be taxed as ordinary income. If you accumulate $1,000,000 in a SEP-IRA by retirement and withdraw $60,000 per year, that entire $60,000 is taxable income each year.

With a Roth IRA alongside your pre-tax accounts, you gain the ability to strategically draw from tax-free funds in retirement. This can keep your taxable income in a lower bracket, reduce your Medicare premiums (which are income-tested), minimize taxes on Social Security benefits, and provide tax-free funds for large unexpected expenses.

Tax diversification — having both pre-tax and after-tax retirement assets — gives you flexibility that a single account type cannot provide.

The Flexibility Advantage: Roth as an Emergency Backup

One of the most underappreciated features of the Roth IRA is that contributions — not earnings — can be withdrawn at any time, for any reason, without tax or penalty. Only earnings are subject to the age and five-year rules.

This means that for a freelancer with $35,000 in Roth IRA contributions, that $35,000 is accessible in a financial emergency without the 10 percent early withdrawal penalty that applies to pre-tax accounts. The Roth IRA effectively functions as a secondary emergency fund that simultaneously builds retirement wealth.

This feature is especially valuable for freelancers who may face income gaps, slow business periods, or unexpected expenses and want maximum financial flexibility.

Roth IRA vs Roth Solo 401(k): Which Is Better?

If your Solo 401(k) provider offers a Roth option, you can make Roth contributions at the full $23,000 employee contribution limit — more than three times the $7,000 Roth IRA limit. For freelancers who want to maximize tax-free retirement savings, using both a Roth Solo 401(k) for the employee contribution and a traditional Roth IRA can be an excellent combined strategy.

The Roth IRA has one advantage the Roth Solo 401(k) does not: there are no required minimum distributions (RMDs) during your lifetime. Roth Solo 401(k) accounts are subject to RMDs starting at age 73 (though they can be rolled into a Roth IRA to avoid this).

When a Traditional (Pre-Tax) Contribution Makes More Sense

The Roth IRA is not always the optimal choice. If you are currently in a high tax bracket and expect to be in a significantly lower bracket in retirement, a traditional pre-tax contribution reduces your taxes now at your current high rate and you pay taxes later at a lower rate. The math favors pre-tax contributions when your current tax rate substantially exceeds your expected future tax rate.

For most freelancers with variable income, having both types of accounts provides the flexibility to optimize annually based on your actual income each year.

Step-by-Step: How to Open a Roth IRA

- Choose a brokerage: Fidelity, Vanguard, and Charles Schwab all offer excellent Roth IRAs with no account fees and access to low-cost index funds.

- Complete the online application: Takes approximately 15 minutes. You will need your Social Security Number, bank account information, and basic personal details.

- Fund the account: Transfer up to $7,000 (or $8,000 if 50+) from your bank account.

- Choose your investments: For most freelancers, a target-date fund or a simple three-fund portfolio (US stocks, international stocks, bonds) is an excellent starting point.

- Set up automatic monthly contributions: Automate $583 per month (for the full $7,000 annual limit) so you never have to think about it.

→ Best Retirement Plans for Self-Employed Americans → SEP-IRA vs Solo 401(k) for Freelancers → How Much Should a Freelancer Save for Retirement? → Complete Freelance Finance Guide