How Much Should a Freelancer Save for Retirement? A Practical Guide for 2026

One of the most challenging financial questions freelancers face is how much to save for retirement. Without a company matching your contributions or a defined benefit pension telling you exactly what you will receive, the full responsibility for your retirement security rests entirely on your own decisions. The stakes are high: save too little and you face a difficult retirement; save too aggressively at the expense of current cash flow and you create unnecessary financial stress today.

The good news is that with the right framework and the right accounts, self-employed individuals can build retirement savings that far exceed what most employees accumulate. This guide gives you the tools to set your target, calculate your savings rate, and build a system that works for variable freelance income.

The Starting Point: What Do You Want Retirement to Look Like?

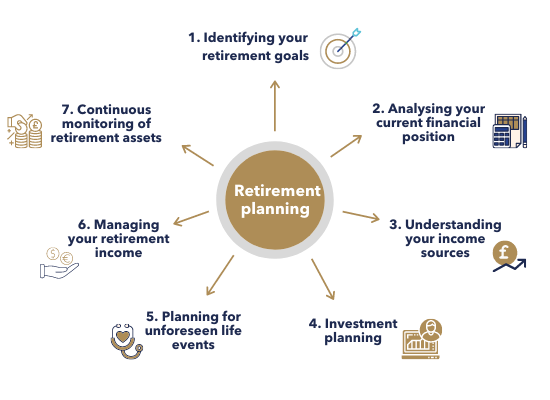

Before calculating how much to save, you need a picture of what you are saving toward. Retirement planning without a target is like navigating without a destination. Consider these questions:

At what age do you want to retire or significantly reduce your working hours? What level of annual income do you want in retirement? Where do you plan to live — a high cost-of-living city, a lower cost rural area, or internationally? Do you expect significant healthcare expenses? Do you want to leave an inheritance or give generously?

Your answers shape every number that follows. A freelancer who wants to retire at 55 in San Francisco with $120,000 per year in income has a very different savings challenge than one who plans to work part-time until 70 in a rural area needing $45,000 per year.

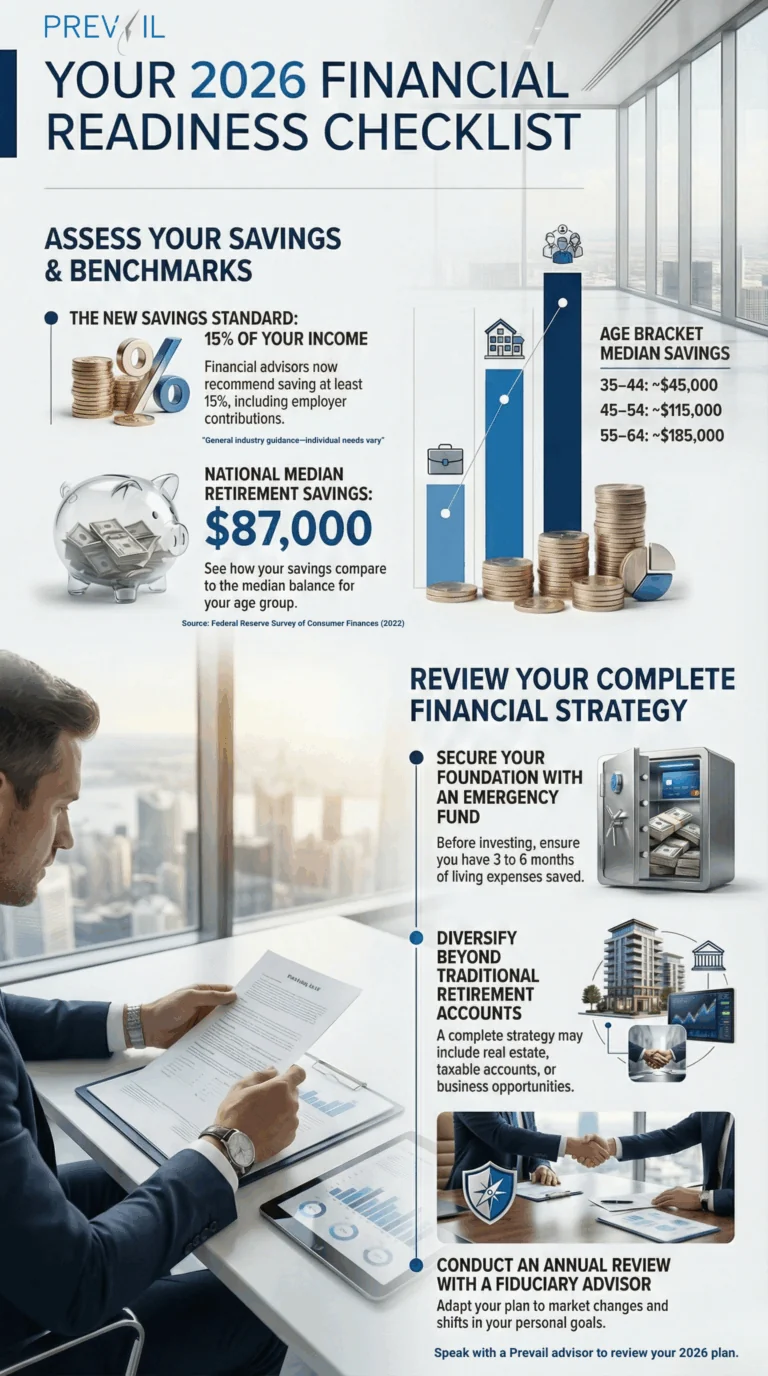

The Classic Savings Rate Guidelines

Several widely used rules of thumb provide a starting framework:

The 10 to 15 percent rule: Save 10 to 15 percent of your gross income for retirement. This works reasonably well if you started saving in your 20s and plan to retire at 65 or later.

The 15 to 20 percent rule for freelancers: Because freelancers receive no employer match and may have lower Social Security benefits due to income variability, most financial planners recommend a savings rate at the higher end — 15 to 20 percent of gross income as a baseline.

The catch-up rules: If you started saving late, add 10 percent to your savings rate for every decade of delay. Starting at 40 instead of 30 means targeting 25 to 30 percent. Starting at 50 means 35 percent or more.

The 25x Rule: How Much Do You Actually Need?

The most widely cited retirement savings target is based on the 4 percent rule, which comes from the Trinity Study and decades of subsequent research on sustainable withdrawal rates. The rule states that a portfolio can sustain annual withdrawals of 4 percent of its starting value for at least 30 years with high probability.

Working backward: if you need $60,000 per year in retirement, you need a portfolio of $1,500,000 ($60,000 divided by 0.04). If you need $80,000 per year, your target is $2,000,000. If you need $40,000 per year, your target is $1,000,000.

This is called the 25x rule: multiply your expected annual retirement spending by 25 to get your savings target.

Important nuances: The 4 percent rule was developed for 30-year retirements. If you plan to retire early — at 50 or 55 — your portfolio needs to last 40 or more years, which may require a lower withdrawal rate of 3 to 3.5 percent and a correspondingly higher savings target (28x to 33x annual spending).

Calculating Your Monthly Savings Requirement

Once you have a target portfolio value and a timeline, you can calculate the monthly contribution needed using compound interest math. Online retirement calculators (Bankrate, Vanguard, and Fidelity all offer excellent free tools) can do this calculation in seconds.

Example: You are 35 years old, have $50,000 already saved, want $1,500,000 by age 65, and expect a 7 percent average annual return. You need to save approximately $1,350 per month to reach your goal. As a freelancer, this is the minimum monthly amount you should be consistently moving into your retirement accounts.

Accounting for Social Security

Freelancers pay the full 15.3 percent self-employment tax, which includes Social Security contributions. This means you are earning Social Security credits and will receive benefits in retirement based on your earnings history.

You can check your estimated Social Security benefit at ssa.gov/myaccount. Use this number as a credit against your retirement income need. If your estimated Social Security benefit is $2,000 per month ($24,000 per year) and you want $80,000 per year in retirement, your portfolio only needs to provide $56,000 per year — reducing your savings target from $2,000,000 to $1,400,000.

However, most financial planners advise treating Social Security as a supplement rather than a cornerstone, given ongoing uncertainty about long-term program sustainability and the fact that benefits can change with legislation.

→ What Is Self-Employment Tax and How to Calculate It

Adjusting for Variable Income

Saving a fixed percentage of income rather than a fixed dollar amount is a practical strategy for freelancers with variable income. In a month where you earn $8,000, you save $1,600 (20 percent). In a month where you earn $4,000, you save $800. Your retirement contribution scales naturally with your income without creating cash flow stress in slow months.

The alternative approach — committing to a fixed monthly retirement contribution — works better in months with higher income but can strain cash flow in slow periods. Many freelancers combine both: a minimum fixed contribution regardless of income (to maintain the habit) and a percentage-based additional contribution in strong months.

The Retirement Savings Priority Order

If you are trying to figure out where to direct limited savings dollars, follow this priority order:

- Emergency fund of three to six months of expenses (absolute first priority)

- Pay quarterly estimated taxes (setting aside 25 to 30 percent of every payment)

- Take advantage of any available retirement tax deductions up to your ability to contribute

- Max out your Roth IRA ($7,000 per year) for tax-free growth

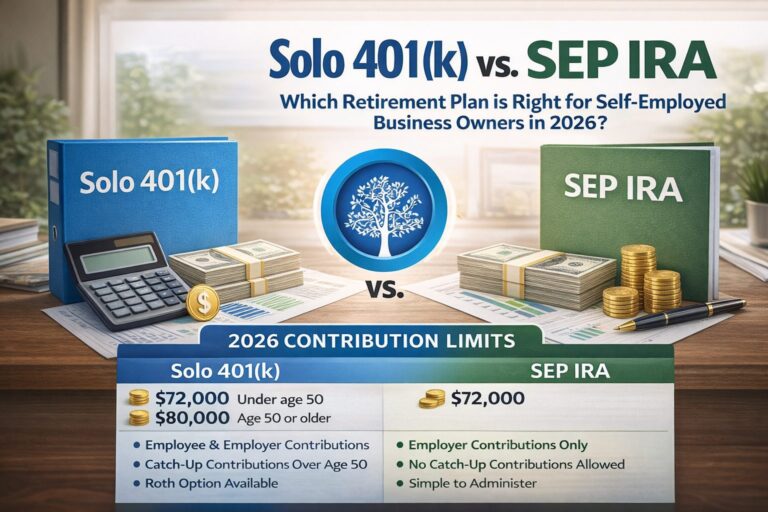

- Max out your SEP-IRA or Solo 401(k) for the current year

- Additional taxable investment accounts if you have reached all other limits

→ How to Budget When Your Income Is Irregular → Best Retirement Plans for Self-Employed Americans → SEP-IRA vs Solo 401(k) for Freelancers → Complete Freelance Finance Guide