Health Insurance for Freelancers Over 50: Best Options and Cost-Saving Strategies

For freelancers over 50, health insurance becomes one of the largest budget items you will face. ACA-compliant plans allow insurers to charge older adults up to three times more than younger adults for the same plan, meaning a plan that costs $400 per month for a 35-year-old can cost $1,000 to $1,200 per month for a 58-year-old. Understanding your options and strategies is essential.

The ACA Age Rating Factor

Under the ACA, insurers can use age as a rating factor, with a maximum ratio of 3:1 between the oldest and youngest adult enrollees. This means premiums for a 64-year-old can be up to three times those for a 21-year-old. For many freelancers in their 50s and early 60s, this makes health insurance a significant monthly expense.

Premium Tax Credits: Especially Valuable for Older Freelancers

The Premium Tax Credit caps the percentage of your income you are required to pay for a benchmark Silver plan. For 2026, most adults with incomes below 400 percent of the federal poverty level (approximately $58,000 for a single adult) pay no more than a capped percentage of income for a Silver plan — the rest is covered by the credit.

For freelancers over 50 who can manage their income below these thresholds — through retirement contributions, for example — the subsidy can be worth thousands of dollars per year.

→ Best Retirement Plans for Self-Employed Americans

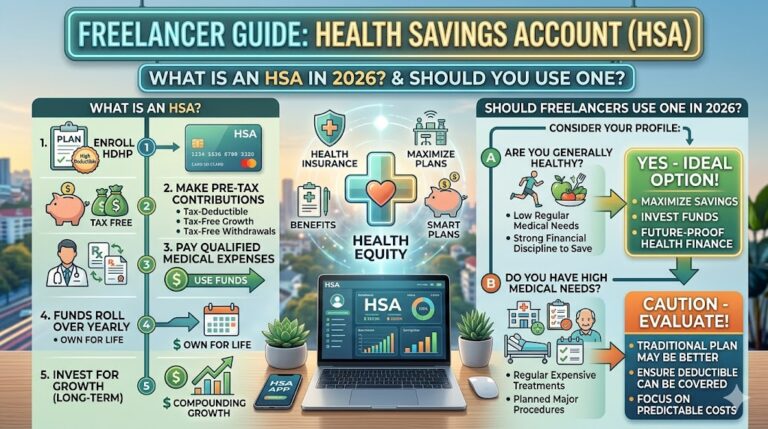

HSA-Eligible High Deductible Plans

A Health Savings Account (HSA) paired with an HSA-eligible high-deductible health plan (HDHP) is a powerful strategy for freelancers over 50. Contributions to an HSA are tax-deductible, grow tax-free, and can be withdrawn tax-free for qualified medical expenses at any time. At age 55, the IRS allows an additional $1,000 catch-up contribution annually.

In 2026, the HSA contribution limit for individual coverage is $4,150 (plus the $1,000 catch-up for those 55 and older). For family coverage, the limit is $8,300 plus the catch-up. These contributions reduce your AGI directly, which can increase your ACA subsidy eligibility.

→ What Is an HSA and Should Freelancers Use One?

Medicare at 65: Planning Ahead

If you are in your 60s, Medicare eligibility at age 65 is a significant financial milestone. Once you enroll in Medicare Part A, you are no longer eligible for an ACA Marketplace plan and lose access to Premium Tax Credits. Planning your transition from Marketplace coverage to Medicare is important to avoid gaps and penalties.

The Late Enrollment Penalty

If you do not enroll in Medicare Part B when you are first eligible at 65, you face a permanent late enrollment penalty of 10 percent for each 12-month period you were eligible but did not enroll. For freelancers who have been managing their own insurance, understanding this deadline is critical.

Bridge Strategies for the 50 to 65 Age Window

For freelancers in the 50 to 65 range, the most effective strategies combine choosing an HSA-eligible plan to build tax-advantaged medical savings, maximizing retirement contributions to manage taxable income and potentially increase subsidy eligibility, and exploring whether your state offers additional low-income healthcare programs.

Comparing Silver vs Gold Plans After 50

At older ages, higher healthcare utilization makes the math on Gold plans more favorable. While Gold plans have higher monthly premiums than Silver plans, the lower deductibles and out-of-pocket maximums often result in lower total annual costs for people who regularly use medical services. Run the numbers for your expected healthcare usage before defaulting to the lowest-premium option.

Working With a Health Insurance Broker

For freelancers over 50 navigating the complexity of ACA subsidies, HSA strategies, and Medicare planning simultaneously, working with a licensed health insurance broker who specializes in the over-50 market is worth considering. Brokers are paid by insurance companies, so their advice costs you nothing directly.

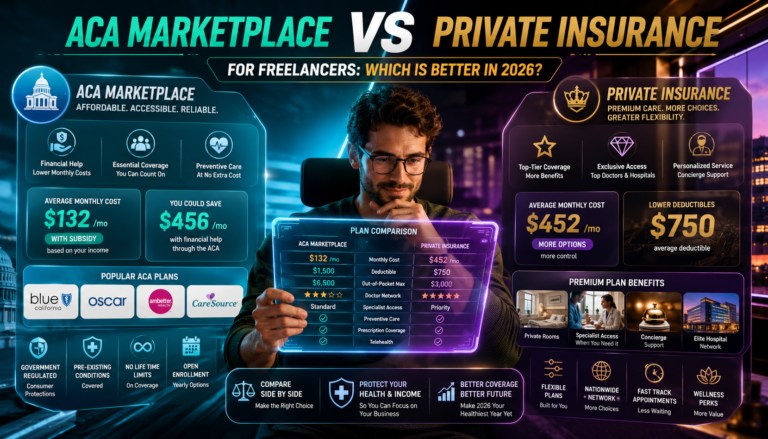

→ Best Health Insurance Plans for Freelancers in the US → How Freelancers Can Deduct Health Insurance Premiums on Taxes → ACA Marketplace vs Private Insurance for Freelancers