Best Health Insurance Plans for Freelancers in the US 2026

Health insurance is arguably the single most stressful financial challenge freelancers face in the United States. Without an employer to cover most of the premium, the full cost of insurance falls on you. But the options available to self-employed Americans in 2026 are broader and more flexible than ever, and with the right strategy, you can find quality coverage at a price that works for your budget.

This guide covers every major health insurance option available to US freelancers, with clear guidance on who each option suits best.

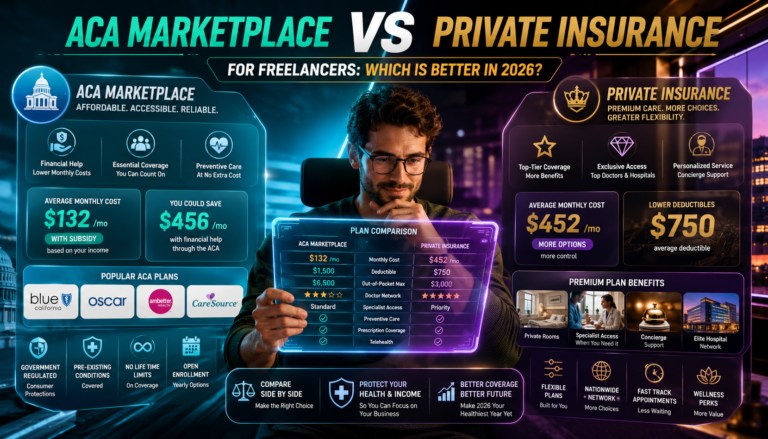

Option 1: ACA Marketplace Plans

The Affordable Care Act (ACA) Marketplace is the most common choice for freelancers. You can enroll during the annual Open Enrollment Period (November 1 to January 15) or at any time if you qualify for a Special Enrollment Period due to a qualifying life event.

The most valuable aspect of ACA plans for freelancers is the Premium Tax Credit, which subsidizes your monthly premiums based on your income. In 2026, Americans earning between 100 percent and 400 percent of the federal poverty level qualify for subsidies, and the American Rescue Plan extended additional subsidies to people above that threshold.

Plans are categorized as Bronze, Silver, Gold, and Platinum based on cost-sharing:

- Bronze: Lowest premium, highest deductible and out-of-pocket costs. Best if you are young and healthy and rarely use medical care.

- Silver: Mid-range premium. Qualifies for Cost-Sharing Reductions (CSRs) if your income is below 250 percent of the poverty level — this is frequently the best value tier.

- Gold: Higher premium, lower deductible. Best if you have regular medical expenses.

- Platinum: Highest premium, lowest cost-sharing. Best for people with significant ongoing healthcare needs.

Option 2: Spouse or Domestic Partner Plan

If your spouse or domestic partner has access to employer-sponsored insurance, joining their plan is often the most cost-effective option. Employer-sponsored plans typically offer lower premiums and better cost-sharing than individual market plans. Check whether your spouse’s employer plan allows dependent enrollment and what the cost difference is between employee-only and employee-plus-spouse coverage.

Option 3: COBRA Continuation Coverage

If you recently left an employer, you can continue your group health coverage for up to 18 months through COBRA. The coverage is identical to your employer plan, but you pay the full premium plus a 2 percent administrative fee. COBRA is often expensive — the average employer plan costs over $7,000 per year for an individual — but it may be worthwhile if you have ongoing medical needs and want coverage continuity while shopping for alternatives.

Option 4: Professional Association Health Plans

Some professional and trade associations offer group health insurance plans to members. Freelancers Union, the National Association of the Self-Employed, and various industry-specific associations offer access to health plans that may be more affordable than individual ACA marketplace options depending on your health history and location.

Option 5: Health Sharing Ministries

Health sharing ministries are faith-based organizations where members share each other’s medical costs. They are not technically insurance and are not regulated like insurance plans. Monthly contributions are typically lower than ACA premiums, but coverage is less comprehensive and can be denied for pre-existing conditions. These plans are suitable only for very healthy individuals who understand and accept the limitations and the faith-based requirements.

How Much Does Health Insurance Cost for Freelancers?

Costs vary enormously based on age, location, plan tier, and income. A 35-year-old in a mid-size US city might pay $350 to $600 per month for a Silver plan before subsidies. With subsidies, costs could drop significantly. A 55-year-old in the same market might pay $700 to $1,200 per month. Always check your state’s ACA Marketplace to get accurate quotes for your specific situation.

The Tax Deduction Angle

Remember that as a self-employed individual, you can deduct 100 percent of your health insurance premiums for yourself and your family. This significantly reduces the effective cost of your coverage.

→ How Freelancers Can Deduct Health Insurance Premiums on Their Taxes → Complete Freelance Finance Guide