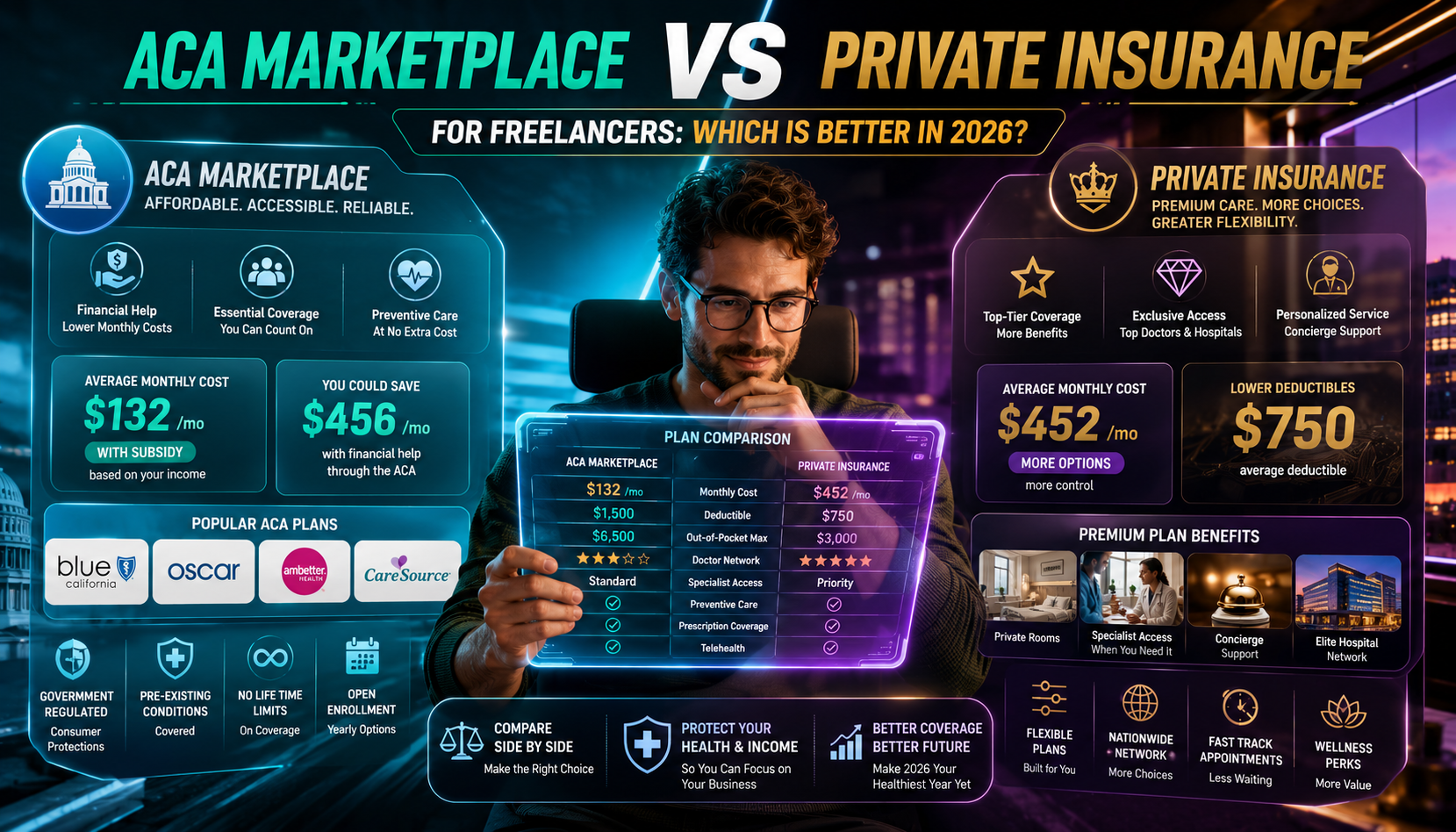

ACA Marketplace vs Private Insurance for Freelancers: Which Is Better in 2026?

When shopping for health insurance as a freelancer, you will encounter two primary markets: the ACA (Affordable Care Act) Marketplace and the private individual health insurance market. Understanding the key differences between these two options is essential for making the right choice for your health and your budget.

What Is the ACA Marketplace?

The ACA Marketplace (also called the Health Insurance Exchange) is a government-facilitated online marketplace where individuals and families can compare and purchase health insurance plans. All plans sold on the Marketplace must meet minimum essential coverage requirements and cannot deny coverage for pre-existing conditions. The defining advantage of Marketplace plans is access to the Premium Tax Credit, which subsidizes monthly premiums for eligible buyers.

What Is Private Individual Health Insurance?

Private health insurance refers to plans sold directly by insurance companies or through brokers outside the ACA Marketplace. These plans include short-term health insurance plans, farm bureau health plans in some states, and traditional individual plans that pre-date ACA requirements.

Key Differences

Pre-existing Conditions

ACA Marketplace plans cannot deny coverage or charge higher premiums based on health history. Private plans, particularly short-term plans, can deny coverage for pre-existing conditions and may exclude them from coverage if you are accepted. This is a critical distinction for anyone with ongoing health conditions.

Premium Tax Credits

Premium Tax Credits are available only for ACA Marketplace plans, not for private plans outside the Marketplace. If your income qualifies you for a significant subsidy, this can make ACA plans dramatically more affordable than private alternatives.

Essential Health Benefits

ACA plans must cover ten essential health benefits including preventive care, mental health services, prescription drugs, maternity care, and emergency services. Private plans, especially short-term plans, may exclude many of these benefits.

Premium Costs

Without subsidies, some private plans may offer lower premiums than ACA plans. However, lower premiums often come with weaker coverage, higher deductibles, and significant coverage gaps. Always compare total potential out-of-pocket costs, not just monthly premiums.

Who Should Choose ACA Marketplace Plans?

- Anyone with pre-existing conditions

- Anyone who qualifies for Premium Tax Credits

- Anyone who wants guaranteed comprehensive coverage

- Freelancers with moderate to high healthcare utilization

Who Might Consider Private Plans?

- Perfectly healthy young freelancers who need a short gap covered (short-term plans only)

- Freelancers whose income is too high to qualify for meaningful ACA subsidies and who want specific plan features

Note: For most freelancers, the ACA Marketplace is the better choice due to the combination of guaranteed coverage, subsidy eligibility, and comprehensive benefits.

Making Your Final Decision

The most important step is to get quotes from both markets for your specific age, location, and income level before making a decision. Healthcare.gov is the starting point for ACA Marketplace quotes in most states. A licensed health insurance broker can help you compare both markets at no additional cost — brokers are paid by the insurance companies, not by you.

The Tax Deduction Reminder

Regardless of which type of plan you choose, your premiums as a self-employed individual are 100 percent deductible from your federal income taxes, reducing the effective monthly cost significantly.

→ Best Health Insurance Plans for Freelancers in the US → How Freelancers Can Deduct Health Insurance Premiums on Taxes → Complete Freelance Finance Guide