Best Bank Accounts for Freelancers in the US 2026: The Complete Guide

Choosing the right bank account is one of the most foundational financial decisions a freelancer makes, yet most new independent workers simply use their personal checking account for everything and wonder why their finances feel chaotic. The truth is that your banking setup is the infrastructure on which every other financial decision rests. Get it right and managing your money becomes almost effortless. Get it wrong and you will spend hours every month untangling personal from business transactions, miss deductions at tax time, and expose yourself to unnecessary legal risk if you operate as an LLC.

This guide covers every aspect of freelancer banking in 2026: why you need separate accounts, which banks offer the best products for self-employed individuals, how many accounts you should have, and how to set up a system that keeps your finances organized automatically.

Why Freelancers Absolutely Need a Dedicated Business Account

Let us start with the most important question: do you actually need a separate business bank account? The short answer is yes, and here is why across four dimensions.

The Tax Dimension

When you file your Schedule C at tax time, you need to report every dollar of business income and every deductible business expense. If personal and business transactions are mixed in the same account, you face a time-consuming sorting process at tax time — scrolling through hundreds of transactions and trying to remember which Amazon purchase was for business and which was personal. With a dedicated business account, every transaction is business-related by definition. Your tax preparation time drops dramatically and your deduction accuracy improves.

The Legal Dimension

If you operate as an LLC, maintaining a strict separation between personal and business finances is not optional — it is legally essential. Commingling personal and business funds is one of the primary ways courts pierce the corporate veil, exposing your personal assets to business liabilities and eliminating the primary protection an LLC provides. Your LLC is only as strong as the financial separation you maintain.

The Clarity Dimension

Knowing exactly how much your business is earning, spending, and profiting requires dedicated accounts. This clarity is essential for good business decisions: whether to raise your rates, take on a new client, invest in equipment, or hire help. Without clear financial data, you are making decisions in the dark.

The Credibility Dimension

Many clients — particularly larger companies — prefer to pay a business entity rather than an individual. A business bank account lets you receive payments made out to your business name. It also simplifies applying for a business credit card and building a business credit profile separate from your personal credit.

→ LLC vs Sole Proprietorship for Freelancers

The Ideal Banking Structure for Freelancers: Three Accounts

The most effective banking system for a freelancer is elegantly simple. You need exactly three accounts, and they serve three distinct purposes.

Account 1 — Business Operating Checking: This is where all client payments arrive and all business expenses are paid. Every invoice you send directs payment here. Every software subscription, equipment purchase, professional development expense, and contractor payment comes out of here. Nothing personal touches this account.

Account 2 — Tax Savings Account: Every time a payment hits your operating account, immediately transfer 25 to 30 percent to this dedicated tax savings account. This money is untouchable until quarterly estimated tax payment dates. Having it in a completely separate account — ideally at a different bank — makes it psychologically harder to spend and eliminates the risk of accidentally using tax money for operating expenses.

Account 3 — Personal Checking: This is your personal account, completely separate from the business. At regular intervals — weekly, biweekly, or monthly — transfer a consistent amount from your business operating account to your personal account as your salary. Everything personal — rent, groceries, personal subscriptions, entertainment — comes out of here.

This three-account structure creates automatic clarity. When you look at your business operating account, everything you see is business. When you look at your personal account, everything is personal. The tax account always has exactly what you owe the IRS set aside and waiting.

→ How to Separate Personal and Business Finances as a Freelancer → How to Budget When Your Income Is Irregular

Best Online Banks for Freelancers in 2026

The best bank accounts for freelancers in 2026 are not at traditional brick-and-mortar banks. Online banks designed specifically for small businesses and independent workers offer superior features, zero fees, and tools that make financial management dramatically easier.

Relay Financial — Best Overall for Freelancers

Relay is purpose-built for small business owners and freelancers, and it shows in every design decision. The standout feature is the ability to create up to 20 individual checking accounts and 2 savings accounts under one login — all for free. This makes implementing the multi-account system described above trivially easy. You can create dedicated accounts for taxes, operating expenses, an emergency buffer, savings for equipment, and anything else you want to track separately.

Relay offers no monthly fees, no minimum balance requirements, and a clean, intuitive interface available on both web and mobile. Integrations with QuickBooks, Xero, and other accounting platforms make bookkeeping seamless. For freelancers who want to implement a Profit First system — where income is immediately allocated into multiple purpose-specific accounts — Relay is the perfect banking infrastructure.

The one limitation: Relay does not pay interest on checking account balances. For your tax savings account where you want the money to grow while waiting for quarterly payment dates, consider keeping it in a separate high-yield savings account.

Mercury — Best for Tech-Oriented Freelancers

Mercury has built an exceptional reputation among tech freelancers, developers, designers, and startup founders. Like Relay, it offers no fees and no minimums with a beautifully designed interface. Mercury stands out for its API access, allowing tech-savvy freelancers to automate financial workflows, and for its virtual card feature, which allows you to create unlimited single-use virtual credit card numbers for online purchases — a useful security feature.

Mercury also offers a high-yield savings account (Mercury Treasury) for balances above $500,000, though for most freelancers the interest on operating account balances is not a differentiating feature.

Mercury integrates smoothly with QuickBooks, Xero, and Stripe, making it an excellent choice for freelancers who bill through multiple payment platforms.

Novo — Best for Freelancers Who Use Multiple Payment Platforms

Novo is designed for small businesses and freelancers with a particular strength in integrations. It connects natively with Stripe, Shopify, Square, PayPal, QuickBooks, Xero, Slack, and many other business tools. If you receive payments through multiple platforms and want all your financial data in one place, Novo’s integration ecosystem is second to none.

No monthly fees, no minimum balance, and a solid mobile app. Novo also offers a useful feature called Reserves — dedicated envelopes within your account for setting aside money for specific purposes, similar in concept to Relay’s multiple accounts but within a single account structure.

Lili — Best for Freelancers Who Want Built-In Tax Tools

Lili is a banking app built specifically for freelancers and the self-employed, with tax management tools built directly into the banking experience. The app automatically categorizes your transactions as business or personal, tracks your deductible expenses throughout the year, and calculates your estimated quarterly tax liability in real time based on your actual income and expenses.

Lili’s Tax Bucket feature automatically sets aside a percentage of every deposit for taxes, eliminating the need for a separate tax savings account. For freelancers who want a single app that handles both banking and basic tax estimation, Lili is a compelling all-in-one option. The free tier is solid, and the premium tier (approximately $17 per month) adds invoicing, receipt scanning, and expanded tax features.

Traditional Banks: When They Make Sense

Despite the advantages of online banks, there are situations where a traditional bank with physical branches makes sense for freelancers:

- You regularly deposit cash or checks and need easy access to branches

- You need a cashier’s check or certified funds for a real estate transaction

- You want the option of face-to-face banking for complex transactions

- Your clients pay by paper check and you want immediate local deposit

If you prefer a traditional bank, the most freelancer-friendly options among major institutions are Chase Business Complete Banking and Bank of America Business Advantage Fundamentals. Both charge monthly fees ($15 to $16) that can be waived by maintaining minimum balances or meeting transaction requirements. Both offer extensive ATM networks and branch access.

What to Look for in a Freelancer Business Account

When evaluating any business bank account, prioritize these features:

Zero or waivable monthly fees: Monthly fees of $15 to $25 add up to $180 to $300 per year — money that should be in your pocket, not the bank’s. Online banks typically offer fee-free accounts as their standard product.

No minimum balance requirements: Freelancers with variable income cannot always maintain high balances. A bank that charges fees when your balance dips below a threshold adds financial stress during slow months.

Free ACH transfers: You will be receiving payments and making transfers constantly. ACH transfers should be free and ideally instant or same-day.

Accounting software integration: Direct connection with QuickBooks, Wave, FreshBooks, or Xero saves hours of manual data entry and reduces categorization errors.

Mobile check deposit: Many freelancers still receive paper checks. Good mobile deposit capability is essential.

Strong customer service: When something goes wrong with a business account — a payment does not arrive, a transaction is disputed — you need responsive support. Check reviews for customer service quality before opening an account.

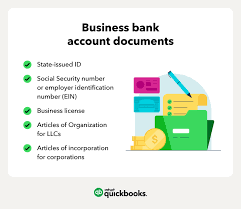

Getting an EIN Before Opening Your Account

Even if you operate as a sole proprietor, apply for an Employer Identification Number (EIN) from the IRS before opening your business bank account. An EIN is a nine-digit business identification number that the IRS issues for free at irs.gov — the online application takes less than ten minutes and you receive your EIN immediately.

Using an EIN instead of your Social Security Number for business banking and credit card applications protects your SSN from exposure and begins building a business credit profile under your business identity. Some banks require an EIN to open a business account; others accept a Social Security Number for sole proprietors.

→ Best Accounting Software for Freelancers 2026 → Do Freelancers Need a Business Bank Account? → Complete Freelance Finance Guide