How to Budget When Your Income Is Irregular: The Complete System for Freelancers

Budgeting on a variable income is one of the most significant financial challenges freelancers face — and one that conventional personal finance advice is completely unprepared to address. Every standard budgeting approach assumes a predictable monthly paycheck. Zero-based budgeting, the 50/30/20 rule, envelope budgeting — all of them are built around the premise that you know what is coming in next month. For a freelancer whose income might range from $2,000 in February to $14,000 in October, these systems simply do not work.

What you need is a fundamentally different approach: a system designed from the ground up for variable income, one that creates stability and predictability in your personal finances regardless of how much your business earns in any given month. This guide gives you that system in full.

Why Traditional Budgets Fail Freelancers

The core problem with traditional monthly budgeting for freelancers is that it treats income as the fixed starting point and expenses as the variable. For employees this is correct — income is fixed and you adjust spending to fit. For freelancers, income is the variable and you need a system that isolates your personal finances from business income volatility.

A freelancer who tries to live month-to-month on their actual monthly income will experience constant financial whiplash: flush with cash in good months, stressed and cutting back in slow months, making emotional financial decisions instead of rational ones. Over time this cycle is exhausting and prevents the consistent savings habits that build long-term wealth.

The solution is to break the direct connection between business income and personal spending.

The Foundation: The Income Buffer Account

The single most important structural element in a freelance financial system is what we call the Income Buffer — a dedicated savings account that sits between your business income and your personal spending. Here is how it works:

All client payments flow into your business operating account. From there, a consistent fixed percentage flows to taxes, a fixed percentage flows to the Income Buffer, and the rest covers business expenses. Your personal account receives a fixed weekly or monthly salary transfer from the Income Buffer — the same amount every time, regardless of how much the business earned.

In good months, the Income Buffer grows. In slow months, it shrinks. But your personal finances never feel the swings because your personal salary is always the same. The Buffer absorbs all the volatility so your lifestyle does not have to.

Target size for the Income Buffer: three to six months of your personal salary. Building this buffer is your first financial priority after establishing your emergency fund.

The Complete Freelancer Budgeting System: Step by Step

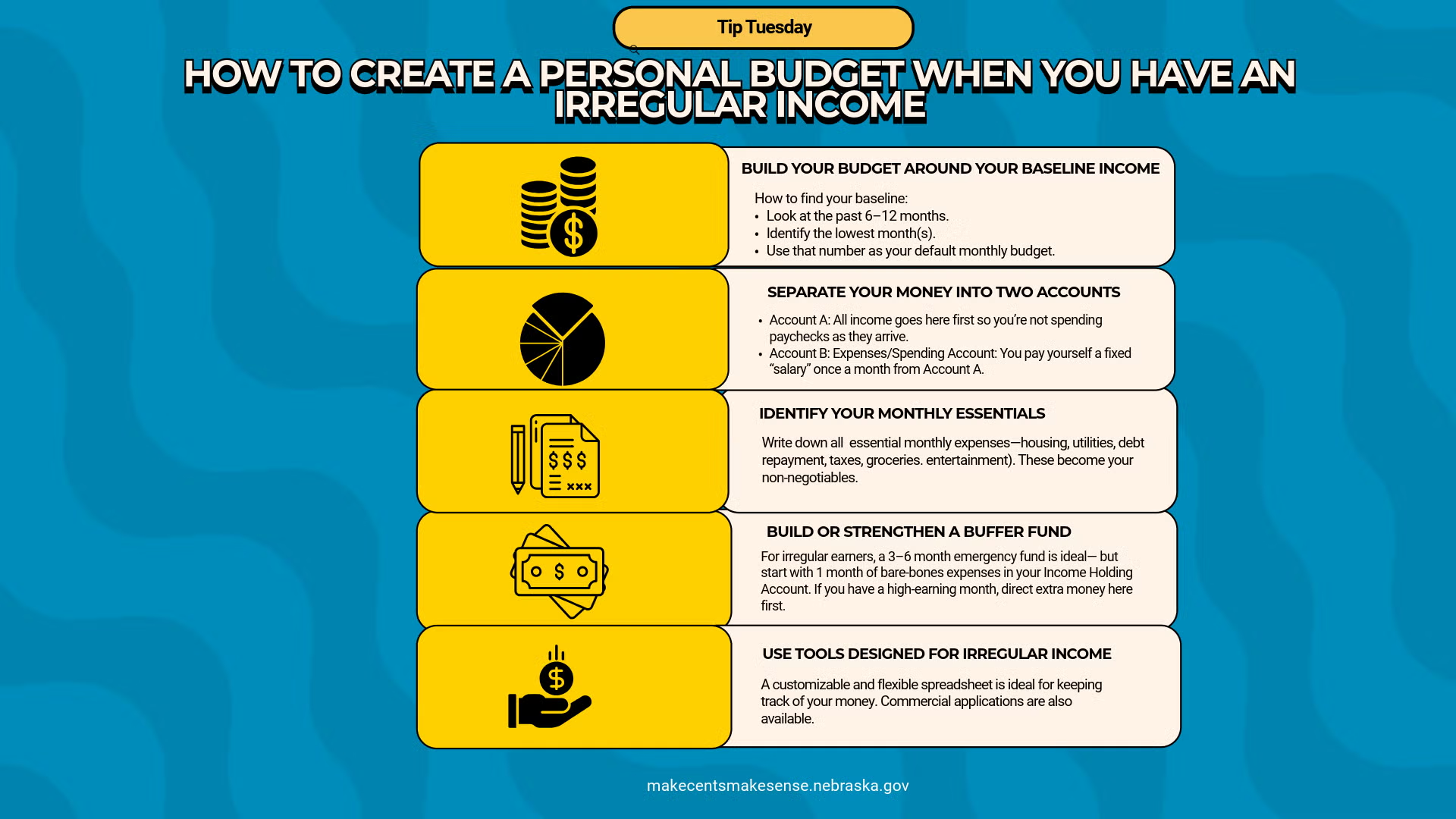

Step 1: Calculate Your Average Monthly Income

Look at your income over the past 12 months (or your best estimate if you are new to freelancing). Add all 12 months and divide by 12. This is your average monthly income — the foundation of everything that follows.

If you are new and have less than 12 months of data, use your most conservative realistic estimate for the year and divide by 12. You can always adjust upward as your actual income becomes clearer.

Step 2: Determine Your Allocation Percentages

Every dollar that comes into your business operating account should be immediately allocated to specific purposes. A framework that works for most freelancers:

25 to 30 percent — Taxes: Transfer this amount to your tax savings account immediately upon receiving any payment. This money is gone. It belongs to the IRS. Treating it this way from the beginning prevents the devastating mistake of spending tax money and then being unable to pay your quarterly obligations.

10 to 15 percent — Income Buffer and Emergency Fund: While building your buffer, direct this allocation to your buffer account. Once the buffer reaches its target size, redirect this percentage to retirement savings or other financial goals.

10 percent — Business Expenses: Keep this available in your operating account for software subscriptions, equipment, marketing, and other operating costs. Adjust based on your actual business expense ratio.

45 to 55 percent — Personal Salary: This is what you pay yourself. Transfer this amount — as a fixed monthly number, not a percentage — to your personal account on a consistent schedule.

Step 3: Set Your Personal Salary at a Conservative Level

Your personal salary should be set at a level your average monthly income can comfortably sustain — not at the level your best months would support. A common guideline is to set your salary at 50 to 60 percent of your average monthly gross income.

For example: if your average monthly gross income is $7,000, your personal salary might be $3,500 to $4,200 per month. This amount arrives in your personal account like clockwork regardless of what the business earned that month. In months where the business earns $12,000, the surplus builds the buffer. In months where the business earns $4,000, the buffer covers the shortfall.

Step 4: Budget Your Personal Account Like an Employee

Once your personal account receives its consistent monthly transfer, you can apply traditional budgeting methods there because the income is now predictable. Apply the 50/30/20 rule, zero-based budgeting, or whatever approach resonates with you. Your personal account behaves just like a salaried employee’s account.

Step 5: Establish a Quarterly Business Review

Rather than reviewing your business finances monthly, conduct a more comprehensive review each quarter. Assess your average income over the past quarter, adjust your salary transfer amount if your income has sustainably increased or decreased, review whether your tax savings rate is adequate based on year-to-date income, and adjust your buffer target if your personal expenses have changed significantly.

The Profit First System: A Popular Alternative

The Profit First methodology, developed by entrepreneur Mike Michalowicz, is a popular variation of the allocation system described above. Its core insight is that profit should be allocated first from every revenue deposit — before paying yourself, before paying expenses — as a way of forcing profitability discipline into your financial system.

The standard Profit First allocation percentages for a freelancer are: 5 percent Profit, 50 percent Owner’s Pay, 15 percent Tax, 30 percent Operating Expenses. These are guidelines, not rigid rules — they should be adjusted based on your actual income level and expense structure.

Many freelancers find Profit First compelling because the act of allocating profit first — even a small amount — creates a psychological commitment to running a profitable business rather than one that consumes all its revenue.

Managing the Feast or Famine Cycle

Every freelancer experiences periods of abundant work followed by periods of drought. The feast-or-famine cycle is not a sign that your business is failing — it is a normal feature of self-employment that can be managed with the right system.

During feast periods: Resist the urge to upgrade your lifestyle. Bank the surplus in your Income Buffer and retirement accounts. Feast periods are when your buffer is built and your retirement savings are accelerated.

During famine periods: Draw from your buffer to maintain your personal salary at its normal level. Avoid making permanent financial decisions — canceling retirement contributions, taking on debt — in response to what is likely a temporary slow period. Review your sales pipeline and intensify client outreach, but do not panic.

The buffer is precisely designed for this purpose. A well-funded buffer of three to six months of personal salary means that even a significant slow period — one where the business earns 50 percent less than normal for two or three months — does not cause personal financial hardship.

What to Do When the Buffer Is Depleted

If a slow period lasts long enough to deplete your Income Buffer, it is time for escalated action. Review your expense structure for anything that can be temporarily reduced. Intensify your client outreach and marketing. Consider taking on short-term or lower-rate projects to generate immediate income. Avoid touching your retirement accounts except as an absolute last resort — the taxes and penalties on early withdrawals are financially devastating.

If business is slow for a sustained period, the underlying issue is likely a client concentration problem (too much revenue from too few clients) or a positioning/marketing issue that the buffer has been masking. Use slow periods as an opportunity to address the structural issues in your business, not just the immediate cash flow gap.

→ Emergency Fund for Freelancers: How Much Do You Need? → Best Bank Accounts for Freelancers in the US → How to Set Your Freelance Rates in the US → Complete Freelance Finance Guide