Emergency Fund for Freelancers: How Much Do You Need and Where to Keep It

The emergency fund is the single most important financial safety net for any freelancer, yet it is consistently the most underbuilt component of freelance financial planning. For employees, an emergency fund protects against job loss, unexpected medical bills, and major home or car repairs. For freelancers, it protects against all of those things plus the unique financial risks of self-employment: a major client suddenly ending a contract, a slow quarter with no new business coming in, a platform shutting down, a health issue that prevents you from working for several weeks, or an equipment failure that halts your ability to deliver work.

The stakes for freelancers are higher than for employees, and the recommended size of the emergency fund reflects that reality. This guide gives you the complete picture: how much you need, how to build it systematically even on a variable income, where to keep it to maximize safety and yield, and how to think about the relationship between your emergency fund and your Income Buffer.

Why Freelancers Need a Larger Emergency Fund Than Employees

The standard personal finance advice for employees is to maintain three to six months of essential living expenses in liquid savings. For freelancers, this baseline is insufficient for several reasons.

No unemployment insurance: If you lose a major client or your business slows dramatically, you are not eligible for state unemployment benefits. There is no government safety net between you and your savings. Every dollar of lost income must be covered by your own reserves.

Income replacement lag: When an employee loses their job, they typically begin the job search immediately and may have a new position within weeks to months. When a freelancer loses a major client, rebuilding that revenue may take months — both to find replacement work and to actually receive payment, since freelance payments typically follow invoicing cycles of 15 to 30 days after work is completed.

Variable income makes emergencies harder to absorb: An employee with a stable paycheck can often absorb a moderate unexpected expense by temporarily cutting discretionary spending. A freelancer who is already experiencing a slow income month has much less flexibility to absorb additional financial shocks.

Business emergencies compound personal emergencies: A freelancer who faces a personal health emergency simultaneously faces a business emergency — they cannot work while recovering, meaning income stops precisely when expenses increase. This double impact requires larger reserves than either issue alone would demand.

For all these reasons, financial planners who work with self-employed clients consistently recommend six months of essential expenses as the minimum target, with nine to twelve months being more appropriate for freelancers in cyclical industries, those with concentrated client bases (where losing one or two clients would eliminate most income), or those with limited ability to rapidly replace lost income.

Calculating Your Emergency Fund Target

The most important principle in sizing your emergency fund is to base it on essential expenses only — not your full current spending. Emergency mode means cutting all discretionary spending: entertainment, dining out, travel, non-essential subscriptions, clothing, and anything else that is a want rather than a need.

Your essential monthly expenses typically include:

Housing: Rent or mortgage payment, renter’s or homeowner’s insurance, property taxes (if not escrowed)

Utilities: Electricity, gas, water, internet (essential for freelancers who work remotely), phone

Food: Groceries only — no restaurant meals in emergency mode

Transportation: Car payment, insurance, fuel, or public transportation costs

Health insurance: This is non-negotiable — do not cancel health insurance to save money in a financial emergency

Minimum debt payments: Minimum payments on any student loans, credit cards, or other debts

Essential business costs: A small number of business expenses that must continue to maintain your ability to earn — your core software subscriptions, your professional liability insurance, your domain and hosting

Add up these essential expenses for a single month. This is your monthly essential expense figure. Multiply by six for the minimum target and by nine or twelve for a more robust target.

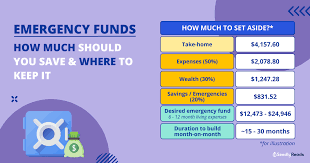

Example: Essential monthly expenses of $3,800 means a six-month emergency fund target of $22,800. At nine months, the target is $34,200. At twelve months, $45,600.

These numbers can feel large and discouraging when you are starting from zero. The antidote is to focus on milestones rather than the final target.

The Milestone Approach to Building Your Emergency Fund

Trying to save six months of expenses in one focused push is demoralizing and impractical for most freelancers managing multiple financial priorities simultaneously. A milestone-based approach makes the goal feel achievable and provides psychological wins along the way.

Milestone 1 — One Month: Your first goal is simply one month of essential expenses. This takes the acute financial panic out of most emergencies. A car repair, a medical bill, a slow week — none of these will derail your finances once you have a one-month buffer in place.

Milestone 2 — Three Months: Three months is the point at which your emergency fund begins to function as a genuine safety net against business disruptions. A slow quarter, the loss of a mid-sized client, or a month-long health issue can be weathered without crisis.

Milestone 3 — Six Months: Six months is the standard recommended target for freelancers. At this level, even a significant business disruption — losing your largest client, a major platform shutting down, or an extended health issue — can be managed without making permanent financial damage.

Milestone 4 — Nine to Twelve Months: If your income is highly concentrated in a small number of clients, if you work in a cyclical industry, or if you have dependents who rely entirely on your income, extending your emergency fund to nine or twelve months provides a level of resilience that allows you to make business decisions from strength rather than desperation.

How to Build Your Emergency Fund on Variable Income

Building savings on a variable income requires a system that works automatically regardless of how much or how little comes in during any given month.

The percentage method: Allocate a fixed percentage of every payment received to the emergency fund. Five percent is a reasonable starting point for most freelancers balancing multiple savings priorities. Ten percent is more aggressive and appropriate if building the emergency fund is your current top financial priority.

The advantage of the percentage method is that it scales with your income. In a month where you earn $8,000, five percent means $400 to the emergency fund. In a month where you earn $3,000, five percent means $150. The contribution adjusts automatically without requiring conscious decisions.

The surplus method: After covering taxes, business expenses, and your personal salary transfer each month, any surplus remaining in your business operating account at the end of the month gets swept to the emergency fund until the target is reached. This method accelerates emergency fund building in strong months without creating pressure in slow months.

The windfall method: Unexpected income — a surprise referral, a project that came in over budget, a tax refund — goes directly to the emergency fund until the target is reached. Windfalls are psychologically the easiest money to save because you were not counting on it.

Most freelancers use a combination of all three approaches simultaneously, which is both practical and effective.

Where to Keep Your Emergency Fund

The emergency fund must satisfy three requirements simultaneously: complete safety of principal (you cannot risk losing any of it), immediate liquidity (you must be able to access it within one business day when needed), and competitive interest yield (it should earn as much as safely possible while sitting idle).

In 2026, high-yield savings accounts at online banks offer the best combination of all three properties. The best available rates at online banks currently range from 4 to 5 percent APY — dramatically better than the 0.01 to 0.5 percent offered by most traditional bank savings accounts.

Top options for emergency fund storage in 2026:

Marcus by Goldman Sachs: Consistently competitive APY with no fees, no minimum balance, and same-day transfers to linked accounts. One of the most reliable options for emergency savings.

Ally Bank Online Savings: No fees, no minimum, competitive APY, and excellent mobile app with bucket features that allow you to organize your savings toward specific goals within one account.

SoFi Savings Account: High APY (often among the top available rates), no fees, and integration with SoFi’s broader financial services. The SoFi app is particularly well-designed for managing multiple savings goals.

Discover Online Savings: Competitive APY with no fees, strong customer service reputation, and an established bank with FDIC insurance on deposits up to $250,000.

What to avoid: Do not keep your emergency fund in a checking account where it earns no interest. Do not invest it in the stock market, bond funds, or any instrument that can lose value — the emergency fund must be available at its full value precisely when you need it most, which may coincide with a market downturn. Do not keep it in certificates of deposit (CDs) with penalties for early withdrawal, which undermines the liquidity requirement.

The Emergency Fund vs the Income Buffer: Understanding the Difference

Many freelancers conflate two distinct financial reserves that serve different purposes and should be kept separate.

The Income Buffer (sometimes called the Operating Buffer) is the reserve in your business account that smooths out month-to-month income variability. When you earn $12,000 in a strong month and transfer a consistent $4,000 personal salary, the extra $8,000 (after taxes and operating expenses) builds the buffer. When you earn $3,000 in a slow month, the buffer covers the normal $4,000 salary transfer. The buffer makes your personal income feel like a steady paycheck regardless of business fluctuations. Target: two to three months of your personal salary in your business operating account.

The Emergency Fund is a completely separate reserve — held outside your business operating account, typically in a personal high-yield savings account — that is reserved exclusively for genuine financial emergencies. It is not touched for slow months (that is what the Income Buffer is for). It is only accessed when an emergency exceeds what the Income Buffer can absorb.

Think of it this way: the Income Buffer handles expected variability. The Emergency Fund handles unexpected crises. Having both is what makes a freelance financial system truly resilient.

What Counts as an Emergency — And What Does Not

Defining what constitutes a legitimate emergency fund draw is important for maintaining the reserve’s integrity. Too broad a definition and you will find yourself depleting it for non-emergencies. Too narrow and you will hesitate to use it when you genuinely need it.

Legitimate emergency fund uses:

- Loss of a major client that eliminates more than 30 percent of your income

- Medical emergency or illness that prevents you from working for two or more weeks

- Major equipment failure that halts your ability to work (computer, camera, specialized equipment)

- Family emergency that requires extended time away from work

- Economic recession that causes widespread client budget cuts

Not legitimate emergency fund uses:

- A slow month covered by the Income Buffer

- An expected annual expense you forgot to plan for (tax bill, insurance renewal)

- A discretionary purchase you did not budget for

- A business investment opportunity

Maintaining this distinction protects the fund’s purpose and ensures it is available at full value when you truly need it.

→ How to Budget When Your Income Is Irregular → Best Bank Accounts for Freelancers in the US → How to Start Saving for Retirement as a New Freelancer → Complete Freelance Finance Guide