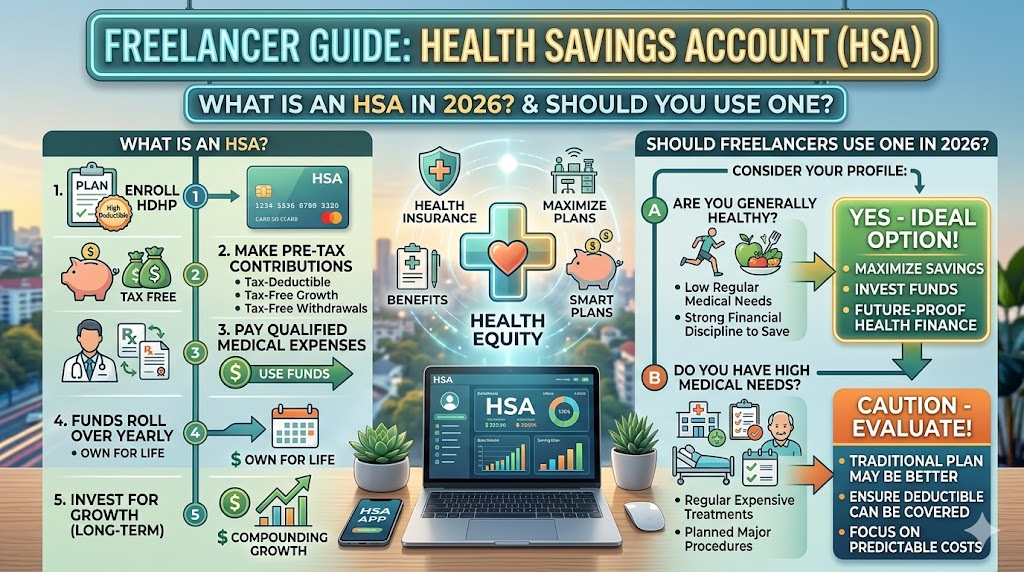

What Is an HSA and Should Freelancers Use One in 2026?

A Health Savings Account (HSA) is one of the most tax-advantaged accounts available to Americans, and freelancers who use an HSA-eligible health plan are uniquely positioned to take full advantage of it. The triple tax benefit — deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses — makes an HSA more tax-efficient than even a 401(k) for healthcare costs.

How an HSA Works

An HSA is a special savings account that can only be opened when you are enrolled in a High Deductible Health Plan (HDHP). You contribute money to the HSA, invest it, and use it for qualified medical expenses. For 2026, you need to be enrolled in a plan with a minimum deductible of $1,600 (individual) or $3,200 (family) to be eligible.

The Triple Tax Advantage

- Contributions are tax-deductible, reducing your AGI

- Money in the HSA grows tax-free (you can invest contributions in mutual funds)

- Withdrawals for qualified medical expenses are completely tax-free

No other account in the US tax code offers this combination. A traditional 401(k) gives you a deduction going in but taxes coming out. A Roth IRA gives you tax-free growth but no deduction going in. An HSA gives you all three benefits simultaneously.

2026 HSA Contribution Limits

- Individual coverage: $4,150

- Family coverage: $8,300

- Catch-up contribution (age 55+): Additional $1,000

Qualified Medical Expenses

HSA funds can be used tax-free for a wide range of expenses including doctor visits, prescription medications, dental care, vision care, mental health services, and many over-the-counter products. As a freelancer who deducts health insurance premiums, HSA funds can also be used for long-term care insurance premiums.

The Pay Now vs Pay Later Strategy

One powerful HSA strategy is to pay current medical expenses out of pocket — without touching your HSA — and let your contributions grow invested in the market. Keep receipts for all medical expenses. Years later, you can reimburse yourself from the HSA for those old expenses, tax-free, with no time limit. This effectively turns your HSA into a tax-free investment account for future use.

HSA as a Retirement Account

After age 65, you can withdraw HSA funds for any purpose — not just medical expenses — without penalty. You will pay ordinary income tax on non-medical withdrawals, making it function exactly like a Traditional IRA. For medical expenses in retirement, which are typically significant, withdrawals remain completely tax-free. This makes the HSA one of the best supplemental retirement savings vehicles available.

How Freelancers Open an HSA

You can open an HSA through many banks, credit unions, and online financial institutions. Fidelity, Lively, and HealthEquity are among the most popular options for investing HSA funds. Your health insurance company may also offer an HSA, though investment options through insurance companies are typically limited.

Is an HDHP Right for You?

The main trade-off of an HSA-eligible plan is the higher deductible. If you have significant ongoing medical expenses, the higher deductible may cost you more out-of-pocket than you save in premiums and tax benefits. Run the numbers for your specific situation before choosing an HDHP. For healthy freelancers with low medical utilization, the math almost always favors the HDHP plus HSA combination.

→ Best Health Insurance Plans for Freelancers in the US → Best Retirement Plans for Self-Employed Americans → How Freelancers Can Deduct Health Insurance Premiums on Taxes